Setting up an investment fund in Luxembourg in 2024 could be a great idea as you will be impressed by all its benefits. As a matter of fact, Luxembourg is known as the largest investment fund center in Europe and the second-largest in the world after the US.

Thus, find out in this article all about opening an investment fund in Luxembourg.

The Tax Authorities consider these undertakings as engaging in investment management activities (like Hedge Funds, Private Equity, or other alternative investments), not commercial activities. Therefore, they are not taxable in Luxembourg.

The CSSF (Commission de Surveillance du Secteur Financier) might consider unregulated partnerships as Alternative Investment Funds. Moreover, these partnerships are subject to annual light reporting without all the AIMFD constraints.

To learn more about investment funds, click here.

The Tax Authorities consider these undertakings as engaging in investment management activities (like Hedge Funds, Private Equity, or other alternative investments), not commercial activities. Therefore, they are not taxable in Luxembourg.

The CSSF (Commission de Surveillance du Secteur Financier) might consider unregulated partnerships as Alternative Investment Funds. Moreover, these partnerships are subject to annual light reporting without all the AIMFD constraints.

To learn more about investment funds, click here.

What are the 3 types of partnerships in Luxembourg?

Following the implementation of AIFMD (Alternative Investment Fund Managers Directive) into Luxembourg law, the rules which apply to Luxembourg limited Partnerships have been adapted to create 3 types of partnerships in Luxembourg:- Common Limited Partnership (Société en Commandite Simple) or CLPs

- Special Limited Partnership (Société en Commandite Spéciale) or SLPs

- Partnerships Limited by Share (Société en Commandite par Actions) or SCA

Special Limited Partnership: a flexible, reliable, and trustworthy solution

The Special Limited Partnerships (SLPs) are used to invest in any type of assets, as a special purpose vehicle (SPV), a co-investment entity for institutional investors, or co-ownership between family offices or HNWIs. People often use SLPs in:- Private Equity Fund

- Venture Capital

- Real Estate Fund

- Reserve Alternative Investment Fund

- and more recently by Hedge Funds

- Crypto Fund

- Art Fund

What about the taxation for a investment fund in Luxembourg?

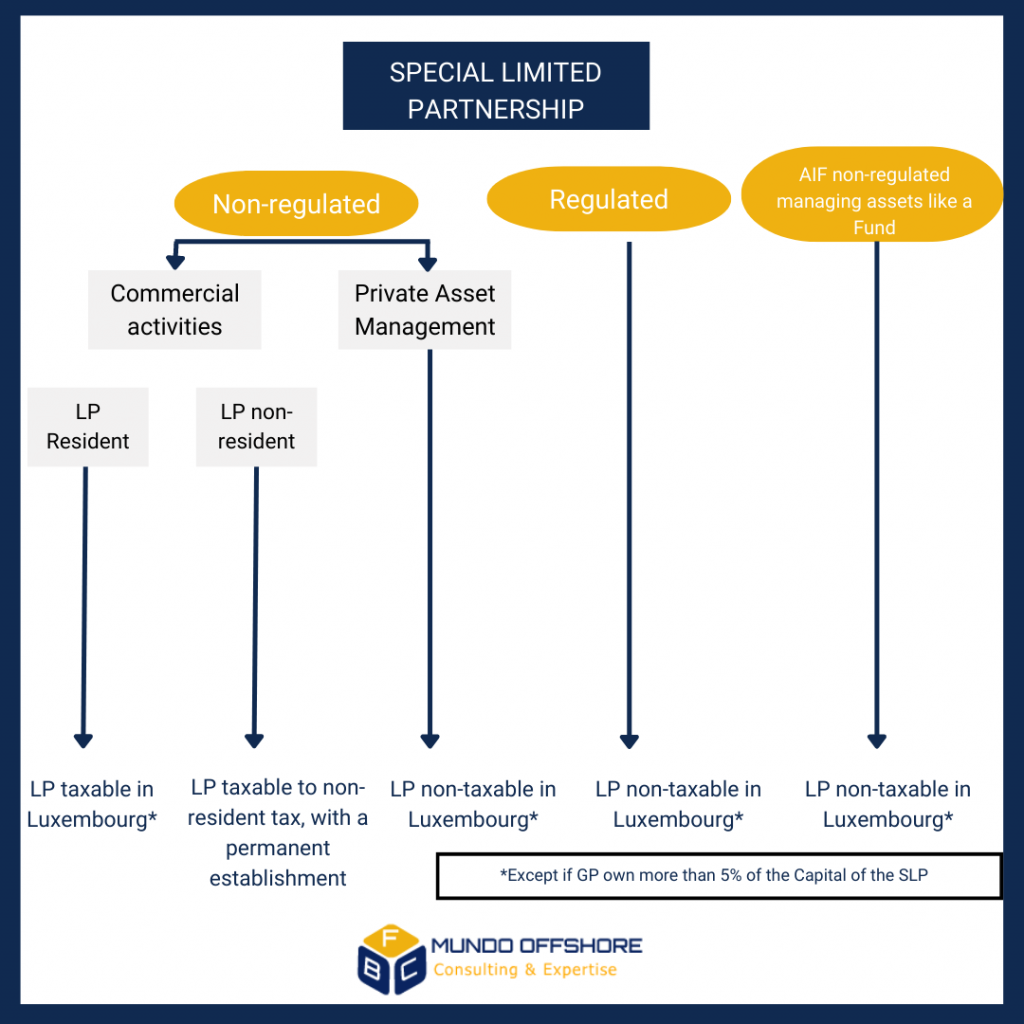

Luxembourg Tax Law (LTL) considers CLP and SLP as tax transparent for income tax purposes. The authorities will grant a tax exemption on the partner’s incomes if the General Partner, a Luxembourg capital company, holds less than 5% of the partnership interests.This is also applicable to municipal business tax. This means that a Partnership will never become taxable itself. Only the Partners of the Partnership may be taxable depending on the conditions mentioned below. The Tax Authorities consider these undertakings as engaging in investment management activities (like Hedge Funds, Private Equity, or other alternative investments), not commercial activities. Therefore, they are not taxable in Luxembourg.

The CSSF (Commission de Surveillance du Secteur Financier) might consider unregulated partnerships as Alternative Investment Funds. Moreover, these partnerships are subject to annual light reporting without all the AIMFD constraints.

To learn more about investment funds, click here.

The Tax Authorities consider these undertakings as engaging in investment management activities (like Hedge Funds, Private Equity, or other alternative investments), not commercial activities. Therefore, they are not taxable in Luxembourg.

The CSSF (Commission de Surveillance du Secteur Financier) might consider unregulated partnerships as Alternative Investment Funds. Moreover, these partnerships are subject to annual light reporting without all the AIMFD constraints.

To learn more about investment funds, click here.